Unintended Consequences of GDP-Weighted Portfolios

Market-cap weighting reflects real-time prices and diversification, while GDP weighting can cause large imbalances and misrepresent investable opportunities.

KEY TAKEAWAYS

- Market-cap weights for securities, industries, and countries provide an instantaneous, continuously updated snapshot of diversification.

- By breaking the link with market prices, gross domestic product (GDP) weighting may lead to sizeable and unwelcome over- or underweights.

- Dimensional believes global portfolios benefit from being well diversified and keeping a strong link to market-cap-based country weights.

With nearly 50 countries to choose from, how does a global equity investor decide where to put each dollar to work?

For a global equity portfolio, weighting by market capitalization is a good place to start. In liquid, competitive capital markets, prices quickly reflect new information and the aggregate expectations of market participants. Hence market-capitalization weights for securities, industries, and countries provide an instantaneous, continuously updated snapshot of diversification. Consider the implications of tariffs or geopolitical tensions. Such impacts are evaluated in real time by global market participants and reflected in the market prices of securities, and therefore in market-cap weights of securities and countries.

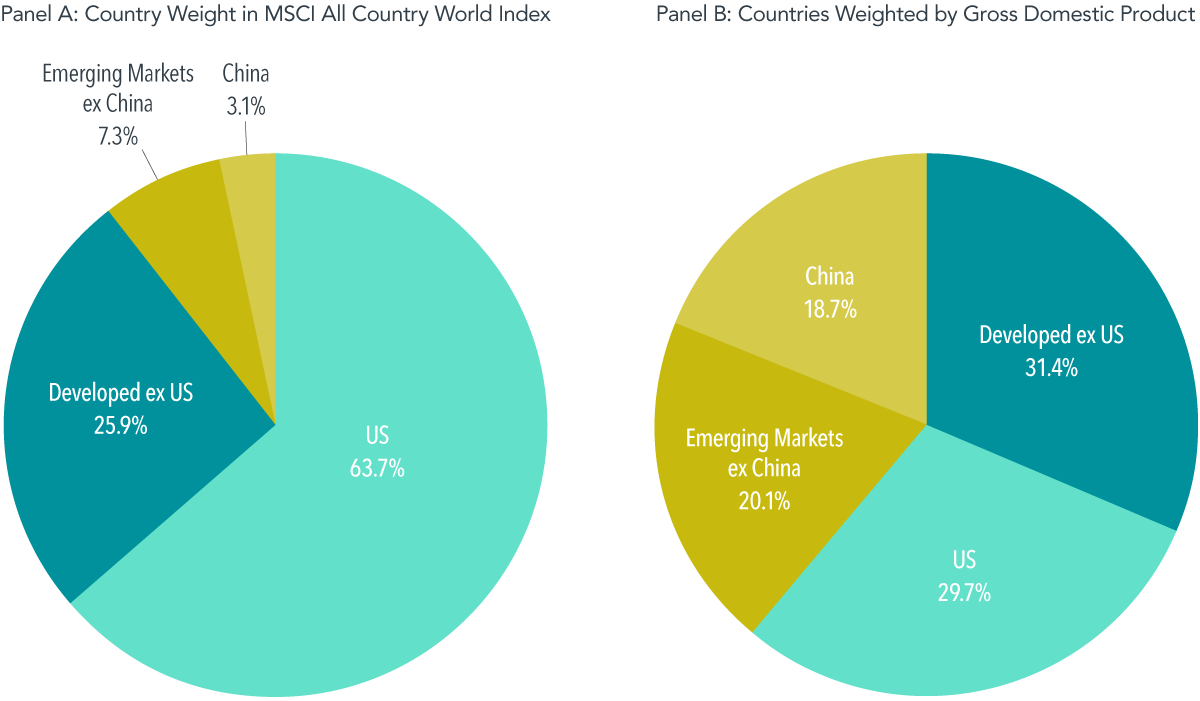

In contrast, weighting by gross domestic product (GDP) is not directly based on a country’s investable opportunity set and, importantly, does not incorporate the information in market prices. This may lead to sizeable overweights and underweights relative to market-capitalization weights. For example, as of April 2025, the MSCI All Country World Index (MSCI ACWI) had a 3.1% allocation to China, compared to 18.7% in a portfolio of MSCI ACWI countries weighted instead by GDP (see Exhibit 1). This overweight to China means four of the top 10 holdings in the MSCI AWCI GDP Weighted Index are Chinese companies, which make up 7.0% of the index versus 1.1% in the MSCI ACWI.1

EXHIBIT 1

World Market Breakdown as of April 30, 2025

There are also practical limitations to building an efficient GDP-weighted portfolio. GDP data are lagged and are often restated, whereas a country’s market capitalization is continuously updated and incorporates new information as it comes out (including information about GDP or restated GDP). In addition, a country can have a large GDP but only a small set of publicly traded stocks, making it challenging to invest a lot in that market. For example, Italy ranks as the eighth-largest country by GDP among the 47 countries in the MSCI ACWI, but Italian stocks account for only 26 of the 2,557 names in the index.2

Using market-capitalization weights as a starting point can also reduce turnover, which can help keep down unnecessary trading costs. In a market-cap-weighting scheme, country weights naturally adjust with relative stock market movements, while other country weighting schemes are likely to incur additional turnover when rebalancing. For example, over the one-year period ending in April 2025, the annual turnover of the MSCI ACWI GDP Weighted Index was 8.3%, over three times higher than the turnover of the MSCI ACWI at 2.6%.

Regardless of weighting scheme, investors might hope to invest in only the best-performing countries. But there is no compelling evidence that country returns can be predicted consistently. While country allocation differences may lead to return differences, especially over the short term, they are not expected to be a reliable return driver over the long run.3 Instead, allocating portfolios using security-level information along with diversification considerations appears to be a more viable approach to pursuing higher expected returns.4

The weaknesses of a GDP-based weighting schema are likely to hold true for other portfolios that ignore or substantially deviate from market weights when determining country weights. While some investors may have a specific reason to deviate from market-cap weights—to overweight securities with higher expected returns, for example, or to accommodate individual preferences or tax considerations—we believe global portfolios benefit from being well diversified and keeping a strong link to market weights when determining country allocations.

Footnotes

1. The MSCI All Country World Index (ACWI) weights countries based on their market capitalization, and the MSCI ACWI GDP Weighted Index (ACWI GDP) has the same eligible universe but weights countries by their GDP. MSCI data © MSCI 2025, all rights reserved.

2. Market-cap-weighted portfolio is based on the MSCI All Country World Index (MSCI ACWI) as of April 30, 2025. GDP-weighted portfolio is based on the April 2025 GDP, as reported by IMF, of countries that make up the MSCI ACWI as of April 30, 2025.

3. Equity premiums have not been related to macroeconomic variables such as GDP growth or country debt. See, for example, “Under the Macroscope: When Stocks and the Economy Diverge” (research paper, Dimensional Fund Advisors, May 2020).

4. For example, see: Mia Huang, Mamdouh Medhat, and Audrey Dong, “Few and Far Between: Why Pursuing Premiums at the Industry and Country Levels Does Not Add Value” (white paper, Dimensional Fund Advisors, March 2023).

Disclosures

The information in this material is intended for the recipient’s background information and use only. It is provided in good faith and without any warranty or representation as to accuracy or completeness. Information and opinions presented in this material have been obtained or derived from sources believed by Dimensional to be reliable, and Dimensional has reasonable grounds to believe that all factual information herein is true as at the date of this material. It does not constitute investment advice, a recommendation, or an offer of any services or products for sale and is not intended to provide a sufficient basis on which to make an investment decision. Before acting on any information in this document, you should consider whether it is appropriate for your particular circumstances and, if appropriate, seek professional advice. It is the responsibility of any persons wishing to make a purchase to inform themselves of and observe all applicable laws and regulations. Unauthorized reproduction or transmission of this material is strictly prohibited. Dimensional accepts no responsibility for loss arising from the use of the information contained herein.

This material is not directed at any person in any jurisdiction where the availability of this material is prohibited or would subject Dimensional or its products or services to any registration, licensing, or other such legal requirements within the jurisdiction.

“Dimensional” refers to the Dimensional separate but affiliated entities generally, rather than to one particular entity. These entities are Dimensional Fund Advisors LP, Dimensional Fund Advisors Ltd., Dimensional Ireland Limited, DFA Australia Limited, Dimensional Fund Advisors Canada ULC, Dimensional Fund Advisors Pte. Ltd., Dimensional Japan Ltd., and Dimensional Hong Kong Limited. Dimensional Hong Kong Limited is licensed by the Securities and Futures Commission to conduct Type 1 (dealing in securities) regulated activities only and does not provide asset management services.

RISKS

Investments involve risks. The investment return and principal value of an investment may fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original value. Past performance is not a guarantee of future results. There is no guarantee strategies will be successful.

CANADA

These materials have been prepared by Dimensional Fund Advisors Canada ULC. The other Dimensional entities referenced herein are not registered resident investment fund managers or portfolio managers in Canada.

This material is not intended for Quebec residents.

Commissions, trailing commissions, management fees, and expenses all may be associated with mutual fund investments. Please read the prospectus before investing. Unless otherwise noted, any indicated total rates of return reflect the historical annual compounded total returns, including changes in share or unit value and reinvestment of all dividends or other distributions, and do not take into account sales, redemption, distribution, or optional charges or income taxes payable by any security holder that would have reduced returns. Mutual funds are not guaranteed, their values change frequently, and past performance may not be repeated.

Resources