Confusing Economic Signs

Dispersion in economic indicators may be responsible for investors’ differing views on where the economy is headed.

Googling “US economy” recently, I got the following headlines as the top two results:

- “US Economy Is Doing Better than Americans Think”

- “Famous Economist Who Predicted 2008 Recession Issues VERY Grim Warning over Future of the US Economy”

Such is the challenge in evaluating the health of the economy in real time. Economic indicators, unlike markets, are backward-looking. The National Bureau of Economic Research (NBER) tends to declare recessions on a lag. The 2020 recession was declared in June, but later determined to have ended in April—two full months before the start was announced.

Part of the uncertainty may stem from the fact that not all economic measures go south during a recession. For example, recessions are usually associated with negative GDP growth, but GDP changes were positive on average during some recessions, such as the ones starting in 1960 and 2001. High unemployment is also considered characteristic of a recession, and yet four of the recessions since 1950 had unemployment below 6%.1 Investors’ views on where the economy is headed may hinge on how much weight they give to different indicators.

There’s also dispersion in opinions about these indicators.2 The median projection for GDP growth by the end of 2024 is 2.6%, which is actually up slightly from the last survey at 2.5%. But the range of projections is substantial. Some analysts gave a nonzero probability to GDP growth coming in below –5%. On the other end of the spectrum, GDP growth over 9% was viewed as plausible. Most analysts revised upward their expectation for unemployment—median projection went from 3.9% to 4.1% between surveys—but with a similarly wide range.

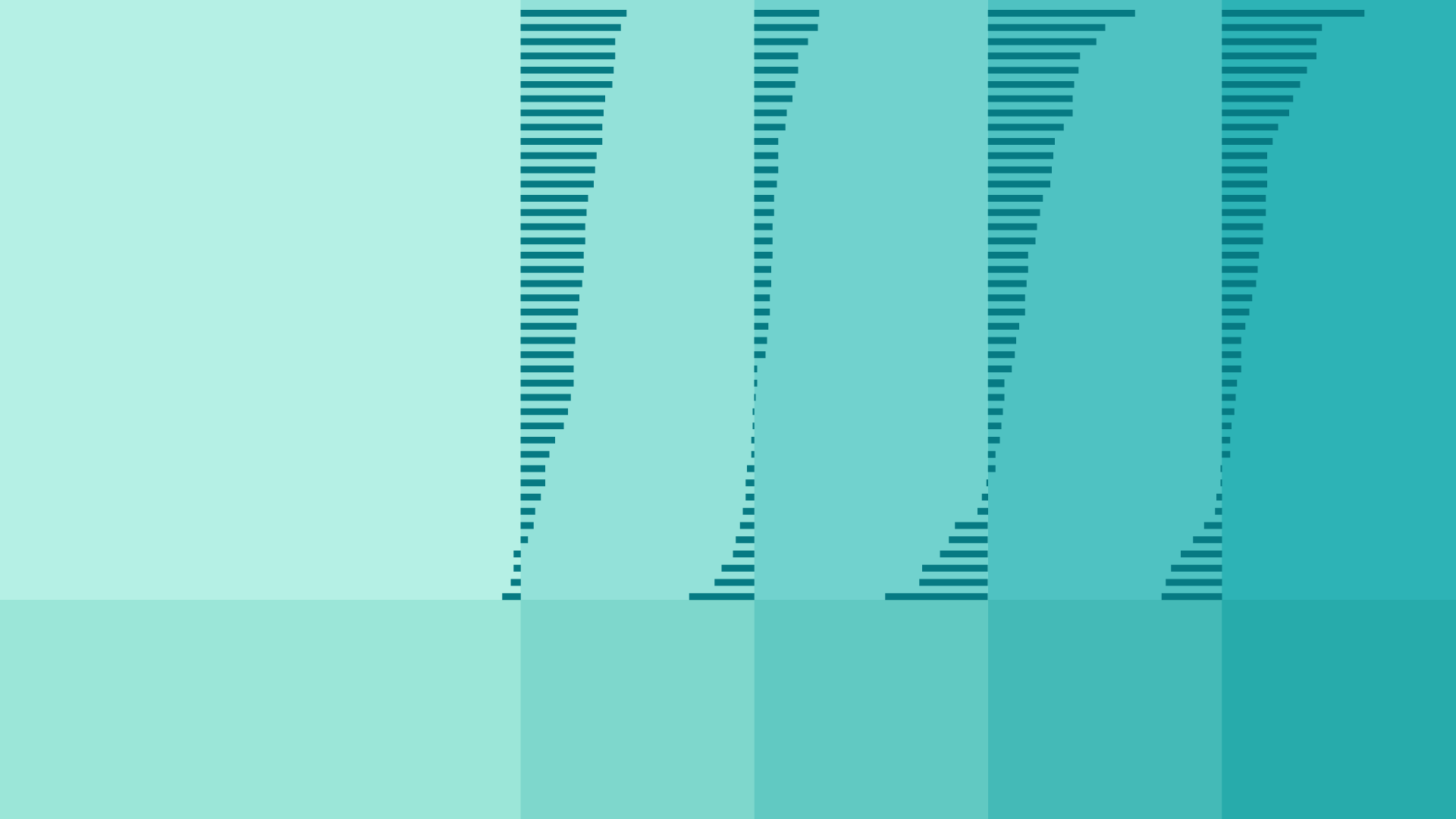

Finally, even if you fall in the camp that is pessimistic about the economy, the history of markets shows that stock returns have often been positive during recessions—the cumulative return on the US market was positive in 12 out of 16 two-year periods that began at the onset of a recession.3

EXHIBIT 1

Conflicting Messages

Google search screenshot from August 26, 2024

Cumulative return shows the growth of a hypothetical investment of $10,000 in the securities in the Fama/French Total US Market Research Index over the 24 months starting the month after the relevant recession start date. The sample includes 16 recessions as identified by NBER from October 1926 to February 2020. NBER defines recessions as starting at the peak of a business cycle.

Index Descriptions

Fama/French Total US Market Research Index: July 1926–present: Fama/French Total US Market Research Factor + One-Month US Treasury Bills. Source: Kenneth R. French - Data Library (dartmouth.edu).

Results shown during periods prior to each index’s inception date do not represent actual returns of the respective index. Other periods selected may have different results, including losses. Backtested index performance is hypothetical and is provided for informational purposes only to indicate historical performance had the index been calculated over the relevant time periods. Backtested performance results assume the reinvestment of dividends and capital gains. Profitability is measured as operating income before depreciation and amortization minus interest expense scaled by book. Eugene Fama and Ken French are members of the Board of Directors of the general partner of, and provide consulting services to, Dimensional Fund Advisors LP.

Footnotes

1. Gross domestic product (GDP) is based on quarterly data from the US Bureau of Economic Analysis; quarterly data is not available prior to 1947. Percentage change in GDP is based on the business cycle peak to trough quarter as reported by NBER. Industrial production, inflation, and unemployment are based on monthly data from the Federal Reserve Bank of St. Louis (FRED); unemployment data is not reported prior to 1929.

2. “Third Quarter 2024 Survey of Professional Forecasters,” Federal Reserve Bank of Philadelphia, August 9, 2024.

3. Past performance is no guarantee of future results. In USD. Performance includes reinvestment of dividends and capital gains. The Fama/French indices represent academic concepts that may be used in portfolio construction and are not available for direct investment or for use as a benchmark. Index returns are not representative of actual portfolios and do not reflect costs and fees associated with an actual investment. See “Index Descriptions” for descriptions of the Dimensional and Fama/French index data.

Disclosures

The information in this material is intended for the recipient’s background information and use only. It is provided in good faith and without any warranty or representation as to accuracy or completeness. Information and opinions presented in this material have been obtained or derived from sources believed by Dimensional to be reliable, and Dimensional has reasonable grounds to believe that all factual information herein is true as at the date of this material. It does not constitute investment advice, a recommendation, or an offer of any services or products for sale and is not intended to provide a sufficient basis on which to make an investment decision. Before acting on any information in this document, you should consider whether it is appropriate for your particular circumstances and, if appropriate, seek professional advice. It is the responsibility of any persons wishing to make a purchase to inform themselves of and observe all applicable laws and regulations. Unauthorized reproduction or transmission of this material is strictly prohibited. Dimensional accepts no responsibility for loss arising from the use of the information contained herein.

This material is not directed at any person in any jurisdiction where the availability of this material is prohibited or would subject Dimensional or its products or services to any registration, licensing, or other such legal requirements within the jurisdiction.

“Dimensional” refers to the Dimensional separate but affiliated entities generally, rather than to one particular entity. These entities are Dimensional Fund Advisors LP, Dimensional Fund Advisors Ltd., Dimensional Ireland Limited, DFA Australia Limited, Dimensional Fund Advisors Canada ULC, Dimensional Fund Advisors Pte. Ltd., Dimensional Japan Ltd., and Dimensional Hong Kong Limited. Dimensional Hong Kong Limited is licensed by the Securities and Futures Commission to conduct Type 1 (dealing in securities) regulated activities only and does not provide asset management services.

RISKS

Investments involve risks. The investment return and principal value of an investment may fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original value. Past performance is not a guarantee of future results. There is no guarantee strategies will be successful.

CANADA

These materials have been prepared by Dimensional Fund Advisors Canada ULC. The other Dimensional entities referenced herein are not registered resident investment fund managers or portfolio managers in Canada.

This material is not intended for Quebec residents.

Commissions, trailing commissions, management fees, and expenses all may be associated with mutual fund investments. Please read the prospectus before investing. Unless otherwise noted, any indicated total rates of return reflect the historical annual compounded total returns, including changes in share or unit value and reinvestment of all dividends or other distributions, and do not take into account sales, redemption, distribution, or optional charges or income taxes payable by any security holder that would have reduced returns. Mutual funds are not guaranteed, their values change frequently, and past performance may not be repeated.

Resources